Understanding MOHELA

MOHELA (MyFedLoan Servicing, LLC) is a loan servicer that manages federal student loans on behalf of the U.S. Department of Education. MOHELA provides various loan services, including loan forbearance, which allows borrowers to temporarily pause their loan payments.

What is Loan Forbearance?

Loan forbearance is a grace period during which borrowers can suspend their student loan payments for a specified duration. This can provide temporary financial relief to borrowers facing hardships such as job loss, medical emergencies, or financial difficulties.

Eligibility for MOHELA Loan Forbearance

To qualify for MOHELA loan forbearance, borrowers must meet certain requirements:

- Be in default or facing financial hardship

- Have made at least 12 consecutive on-time payments prior to requesting forbearance

- Not be in forbearance status for more than 3 years over the life of the loan

Types of MOHELA Forbearance

MOHELA offers two types of forbearance:

- Economic Hardship Forbearance: Allows borrowers to pause payments for up to 36 months due to financial difficulties, such as job loss or medical expenses.

- Military Forbearance: Provides payment suspension for borrowers who are actively serving in the military.

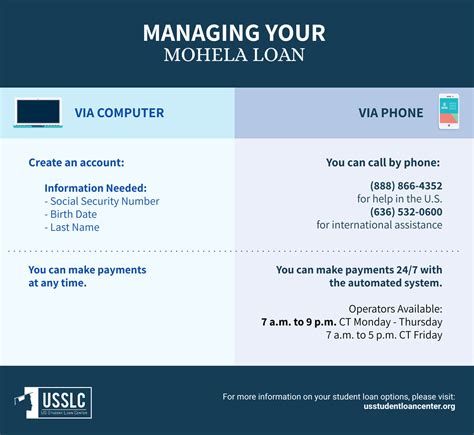

Applying for MOHELA Loan Forbearance

Borrowers can apply for MOHELA loan forbearance online, via phone, or by mail:

- Online: Log in to your MOHELA account and navigate to the “Forbearance” section.

- Phone: Call MOHELA at 1-888-866-3342.

- Mail: Send a written request to: MOHELA, P.O. Box 5550, Harrisburg, PA 17110-5550.

Consequences of Loan Forbearance

While loan forbearance can provide temporary relief, it’s important to understand its potential consequences:

- Interest Accrual: Interest continues to accrue during forbearance, so the total loan balance will increase.

- Extended Repayment Period: Forbearance extends the life of the loan, meaning it will take longer to repay.

- Negative Impact on Credit Score: Forbearance may be reported on a borrower’s credit report and impact their credit score.

Alternative Options to Forbearance

Depending on the borrower’s financial situation, there may be alternative options to forbearance:

- Income-Driven Repayment Plan: This plan adjusts loan payments based on income and family size, resulting in lower monthly payments.

- Loan Consolidation: Combining multiple student loans into one loan with a lower interest rate and extended repayment period.

- Loan Discharge: In certain cases, such as permanent disability or loan forgiveness programs, borrowers may be eligible to have their student loans discharged.

Tips and Tricks for Negotiating with MOHELA

- Be prepared: Gather documentation to support your financial hardship or other eligibility requirements.

- Communicate proactively: Reach out to MOHELA and explain your situation clearly and concisely.

- Negotiate a favorable term: Discuss the length of forbearance, interest rate adjustment, and any additional options available.

- Document your agreements: Get everything in writing to avoid misunderstandings or disputes.

Common Mistakes to Avoid

- Delaying the Application: Apply for forbearance as soon as possible to minimize interest accrual and potential damage to your credit.

- Not Providing Documentation: Failure to provide supporting documents can result in your forbearance request being denied.

- Ignoring Payments after Forbearance: Resuming payments on time after forbearance ends is crucial to avoid default.

- Overestimating the Benefits: Forbearance is a temporary solution and should not be used as a long-term financial strategy.

Conclusion

MOHELA loan forbearance can provide borrowers with temporary financial relief during periods of hardship. However, it’s essential to understand the consequences and explore alternative options before making a decision. By following the tips and avoiding common mistakes, borrowers can effectively negotiate with MOHELA and navigate the forbearance process successfully.