Introduction

The realms of economics and business are intertwined yet distinct, shaping our financial landscape and influencing our daily lives. Economics, the study of production, distribution, and consumption of goods and services, provides the foundational principles that guide business decision-making. Business, on the other hand, translates economic theories into practical strategies that drive enterprise. This article delves into the nuances of economics and business, exploring their interconnectedness and the value each brings to the world of commerce.

The Scope of Economics

Economics encompasses a broad spectrum of concepts and theories that analyze how individuals and societies allocate scarce resources to satisfy their wants and needs. It investigates the following key areas:

- Microeconomics: Examines individual decision-making by consumers and businesses and how they interact in specific markets.

- Macroeconomics: Analyzes the economy as a whole, encompassing factors such as inflation, unemployment, and economic growth.

- International Economics: Explores the interactions between different countries and their economic systems, including trade, exchange rates, and global finance.

The Role of Business

Business, while rooted in economic principles, focuses on specific organizational objectives. It involves the following core functions:

- Production: Creating goods or services that meet market demand.

- Marketing: Promoting and distributing products or services to customers.

- Finance: Managing the financial resources needed to operate and grow the business.

- Human Resources: Managing employees and creating a positive work environment.

- Strategy: Developing and executing long-term plans to achieve business goals.

Interplay between Economics and Business

Economics provides the theoretical framework that informs business decisions. For example:

- Market Analysis: Economic principles help businesses understand market demand, competition, and pricing strategies.

- Resource Allocation: Economics guides businesses in making optimal decisions about resource allocation to maximize profits.

- Economic Forecasting: Economic forecasts help businesses anticipate economic trends and adjust their strategies accordingly.

Business, in turn, drives economic growth. For example:

- Job Creation: Businesses are the primary source of employment, contributing to economic output and job security.

- Innovation: Businesses invest in research and development to introduce new products and services, spurring economic progress.

- Tax Revenue: Business activities generate tax revenue, which governments use to fund public services and infrastructure.

Tables of Key Differences

| Feature | Economics | Business |

|---|---|---|

| Focus | Allocation of scarce resources | Organizational objectives |

| Scope | Economy as a whole, markets, individuals | Specific enterprises |

| Theories | Microeconomics, macroeconomics, international economics | Marketing, finance, human resources, strategy |

| Application | Government policy, economic models | Daily operations, business decisions |

| Impact | Influences economic growth, unemployment, inflation | Generates profits, creates jobs, drives innovation |

| Definition | Description | Examples |

|---|---|---|

| Microeconomics | Examines the behavior of individual consumers, firms, and industries | Demand curve, perfect competition, elasticity |

| Macroeconomics | Analyzes the economy as a whole | Gross domestic product (GDP), inflation, unemployment |

| International Economics | Studies economic relationships between countries | Trade agreements, foreign exchange, global supply chains |

| Production | Creating goods or services | Manufacturing, software development, agricultural farming |

| Marketing | Promoting and distributing products or services | Advertising, public relations, social media marketing |

| Finance | Managing financial resources | Budgeting, cash flow analysis, investment decisions |

| Human Resources | Managing employees | Recruitment, training, employee relations |

| Strategy | Developing long-term plans | Market segmentation, product differentiation, competitive advantage |

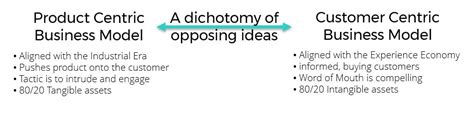

Economics and business share a common goal: Meeting the wants and needs of consumers. Economics analyzes consumer behavior and market dynamics to identify unmet demands. Businesses leverage this knowledge to develop products and services that cater to those needs.

Strategies for Customer-Centricity

- Market Research: Conducting thorough research to understand customer preferences, motivations, and pain points.

- Product Innovation: Developing new products or services that solve customer problems or fulfill unmet desires.

- Exceptional Customer Service: Providing personalized interactions, timely support, and seamless experiences to build customer loyalty.

- Targeted Marketing: Focusing marketing efforts on specific customer segments based on their needs and interests.

- Stay Informed: Monitor economic indicators, industry trends, and customer feedback to make data-driven decisions.

- Scenario Planning: Develop multiple scenarios to anticipate potential economic or business challenges and prepare contingency plans.

- Prioritize Return on Investment (ROI): Evaluate the financial returns of decisions to ensure they align with business objectives.

- Embrace Innovation: Seek out and implement new technologies and practices to enhance efficiency and competitiveness.

- Seek Professional Advice: Consult with economists or business professionals when making complex decisions or facing economic uncertainty.

Economics and business are two sides of the same coin, providing a comprehensive framework for understanding and navigating the world of commerce. Economics lays the foundation by analyzing resource allocation and economic behavior, while business translates these principles into practical strategies. By understanding the interplay between these disciplines, businesses can make informed decisions that drive growth, satisfy customer needs, and contribute to economic prosperity.