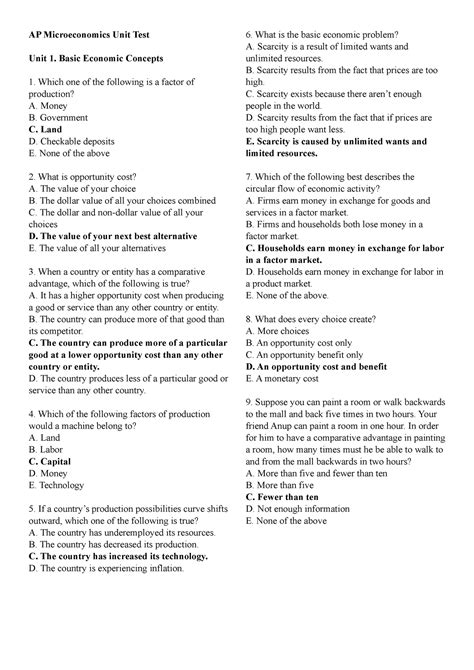

Feeling prepared for the AP Microeconomics Unit 1 exam? Test your knowledge with this comprehensive practice test, covering all the key concepts from the unit.

Multiple Choice

-

The law of demand states that:

(a) As the price of a good increases, so will the quantity demanded.

(b) As the price of a good decreases, so will the quantity demanded.

(c) As the price of a good increases, so will the quantity supplied.

(d) As the price of a good decreases, so will the quantity supplied. -

Which factor would shift the demand curve to the right?

(a) An increase in the price of a substitute good

(b) A decrease in the price of a complementary good

(c) A decrease in consumer income

(d) An increase in consumer taste and preferences -

At the equilibrium price:

(a) Quantity supplied is greater than quantity demanded.

(b) Quantity demanded is greater than quantity supplied.

(c) Quantity supplied is equal to quantity demanded.

(d) Price is at its maximum. -

When the price of a good is below the equilibrium price, there is:

(a) A surplus

(b) A shortage

(c) A price ceiling

(d) A price floor -

A price elasticity of demand of -0.5 indicates that:

(a) Demand is relatively elastic

(b) Demand is relatively inelastic

(c) Demand is perfectly elastic

(d) Demand is perfectly inelastic

Short Answer

- Explain the concept of elasticity.

- Describe the three factors that can shift the supply curve.

- Discuss the effects of a price ceiling on the market for a good.

Free Response

- Analyze the impact of a technological innovation on the equilibrium price and quantity of a good.

- Explain how government regulations can affect the efficiency of a market.

Answer Key

Multiple Choice

1. (b)

2. (d)

3. (c)

4. (b)

5. (b)

Short Answer

1. See textbook for definition of elasticity.

2. See textbook for factors that shift the supply curve.

3. See textbook for effects of a price ceiling.

Free Response

1. See textbook for analysis of a technological innovation.

2. See textbook for effects of government regulations on market efficiency.