The economic landscape is adorned with a diverse array of industries, each characterized by unique production costs and operational dynamics. Among these, constant cost industries stand out as a distinctive category, exhibiting a fascinating interplay between output levels and production expenses.

Characteristics of Constant Cost Industries

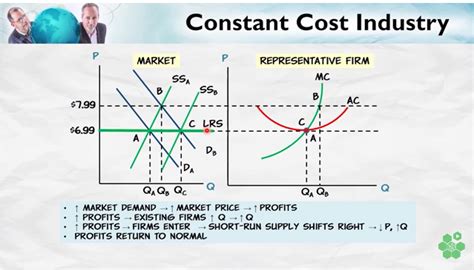

A constant cost industry is defined by its unwavering marginal cost of production. This implies that, as output increases, the additional cost incurred per unit of output remains constant. Unlike industries with increasing or decreasing marginal costs, constant cost industries maintain a consistent cost structure regardless of production volume.

The unwavering nature of marginal costs in constant cost industries can be attributed to several factors, including:

- Availability of Fixed Input Prices: Key inputs, such as raw materials and labor, are available at a constant price, regardless of output levels. This ensures that the cost per unit of output remains stable.

- Fixed Production Technology: The production process does not require significant adjustments or additional resources as output increases. This eliminates the need for costly investments in new machinery or processes.

- Economies of Scale: Constant cost industries often achieve economies of scale, where increased production volume leads to a reduction in fixed costs per unit. This offsets the higher variable costs associated with larger output levels.

Examples of industries exhibiting constant marginal costs include electricity generation, water supply, and telecommunications. In these industries, the cost of producing an additional unit of output is consistently low, allowing for scalable production without significant cost increases.

Implications for Industry Structure

The unique cost structure of constant cost industries has a profound impact on their market dynamics:

- High Fixed Costs: Entry into constant cost industries typically requires high fixed costs, such as investment in infrastructure and equipment. This creates barriers to entry, limiting competition and promoting economies of scale.

- Price Stability: Despite constant marginal costs, prices in constant cost industries may not be perfectly stable. External factors, such as fluctuations in input prices, can affect overall costs and lead to price adjustments.

- Natural Monopolies: Constant cost industries often exhibit natural monopoly characteristics, where a single firm can produce at a lower cost than multiple smaller firms. This can lead to the formation of monopolies or oligopolies, reducing competition and potentially affecting consumer prices.

Benefits and Challenges for Consumers

The unique cost structure of constant cost industries presents both benefits and challenges for consumers:

- Stable Prices: Constant marginal costs can lead to stable prices, reducing consumers’ exposure to price spikes or volatility.

- Availability of Essential Services: Constant cost industries often provide essential services, such as electricity and water, ensuring reliable access to these utilities.

- Potential Monopolization: The potential for natural monopolies can raise concerns about market power and pricing abuses. Consumers may face higher prices or reduced service quality in monopolized markets.

Conclusion

Constant cost industries play a vital role in the economy, providing essential services and contributing to overall market stability. Their unwavering marginal costs allow for scalable production without significant cost increases, leading to economies of scale and potentially lower prices for consumers. However, the high fixed costs associated with entry and the potential for monopolization pose challenges that require careful market regulation and oversight. Understanding the dynamics of constant cost industries is crucial for policymakers, industry participants, and consumers alike to ensure optimal market outcomes.